Swap - equivalent rate for floating leg when reset frequency and payment frequency is not equal

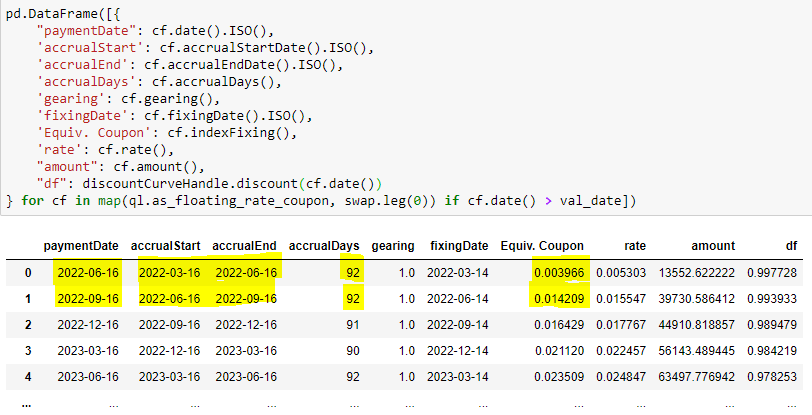

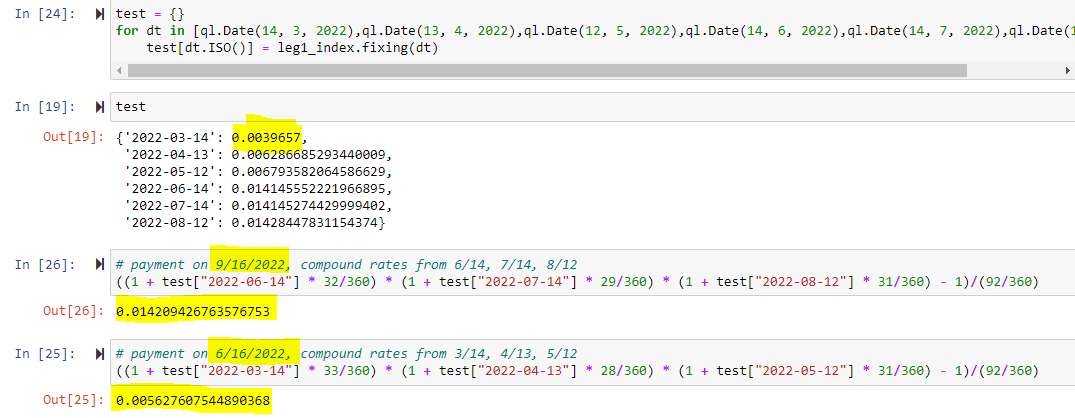

I'm trying to price a swap, and one of the floating legs is referring to 1M LIBOR. The trade start date and valuation date are both March-16, 2022, and the pays quarterly. Theoretically, the equivalent rate should be calculated based on the compounded rate after each reset. I can see that from the 2nd payment onwards, the equivalent rate is as expected; however for the 1st payment, it is simply using the fixing rate from before the accrual start date, instead of the compounded rate. Can anyone please check and see if this is an error?

Thanks for posting! It might take a while before we look at your issue, so don't worry if there seems to be no feedback. We'll get to it.

This issue was automatically marked as stale because it has been open 60 days with no activity. Remove stale label or comment, or this will be closed in two weeks.

Hello, may you post the code you're using to initialize the swap? Thanks!

Float-Float Swap - Quantlib Test.zip

Hello, may you post the code you're using to initialize the swap? Thanks!

Please see the python notebook attached. Thank you.

This issue was automatically marked as stale because it has been open 60 days with no activity. Remove stale label or comment, or this will be closed in two weeks.