pmdarima

pmdarima copied to clipboard

pmdarima copied to clipboard

auto_arima returns flat predictions for near-zero scaled time series

Describe the bug

auto_arima is returning constant predictions when data is too small., i.e., close to zero

Initially, I generated a linear trendy time series with slope 0.5 and intercept 100, plus some noise. Then, I wanted to change units of my data and I divided the values of the time series by $10^6$. I expected to obtain a similar prediction. However, auto_arima returned a repeated constant value that poorly predicts my data.

To Reproduce

This is a sample code that shows the bug

import pmdarima as pm

from sktime.utils.plotting import plot_series

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

#generate data

a, b = 0.5, 100

y1 = a*np.arange(0,100)+b

noise = np.random.normal(y1)

y1 = y1 + noise

y2 = y1 / (10**6)

window = 20

y1_train = pd.Series(y1[:-window], index = pd.Index(np.arange(0, len(y1)-window)))

y1_test = pd.Series(y1[-window:], index = pd.Index(np.arange(len(y1)-window, len(y1))))

y2_train = pd.Series(y2[:-window], index = pd.Index(np.arange(0, len(y2)-window)))

y2_test = pd.Series(y2[-window:], index = pd.Index(np.arange(len(y2)-window, len(y2))))

# Fit your model

model = pm.auto_arima(y1_train)

# make your forecasts

forecasts = model.predict(y1_test.shape[0]) # predict N steps into the future

y1_pred = pd.Series(forecasts, index=y1_test.index)

plot_series(y1_train, y1_test, y1_pred, labels=["train", "test", "pred"])

plt.title("Data and ARIMA forecast before change of scale")

plt.show()

# Fit your model

model = pm.auto_arima(y2_train)

# make your forecasts

forecasts = model.predict(y2_test.shape[0]) # predict N steps into the future

y2_pred = pd.Series(forecasts, index=y2_test.index)

plot_series(y2_train, y2_test, y2_pred, labels=["train", "test", "pred"])

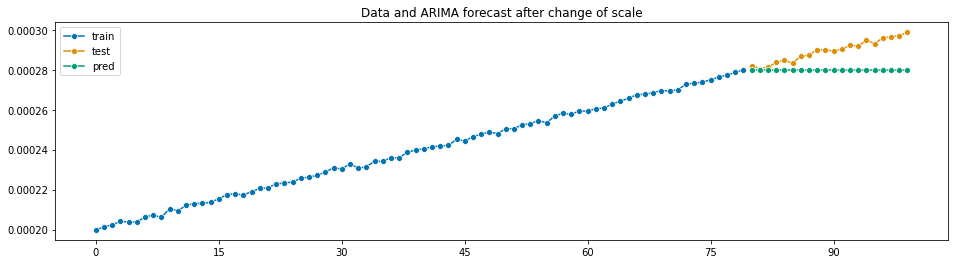

plt.title("Data and ARIMA forecast after change of scale")

plt.show()

The output is:

Versions

/home/claudia/Desktop/debug_pmdarima/lib/python3.8/site-packages/_distutils_hack/__init__.py:30: UserWarning: Setuptools is replacing distutils.

warnings.warn("Setuptools is replacing distutils.")

System:

python: 3.8.10 (default, Nov 26 2021, 20:14:08) [GCC 9.3.0]

executable: /home/claudia/Desktop/debug_pmdarima/bin/python3

machine: Linux-5.13.0-1029-oem-x86_64-with-glibc2.29

Python dependencies:

pip: 21.3.1

setuptools: 60.5.0

sklearn: 1.0.2

statsmodels: 0.13.2

numpy: 1.21.5

scipy: 1.8.0

Cython: 0.29.28

pandas: 1.4.1

joblib: 1.1.0

pmdarima: 1.8.4

Linux-5.13.0-1029-oem-x86_64-with-glibc2.29

Python 3.8.10 (default, Nov 26 2021, 20:14:08)

[GCC 9.3.0]

pmdarima 1.8.4

NumPy 1.21.5

SciPy 1.8.0

Scikit-Learn 1.0.2

Statsmodels 0.13.2

Expected Behavior

I would expect to obtain a similar shape to the one produced in the first forecast

Actual Behavior

auto_arima produces the following forecast:

80 0.00028

81 0.00028

82 0.00028

83 0.00028

84 0.00028

85 0.00028

86 0.00028

87 0.00028

88 0.00028

89 0.00028

90 0.00028

91 0.00028

92 0.00028

93 0.00028

94 0.00028

95 0.00028

96 0.00028

97 0.00028

98 0.00028

99 0.00028

dtype: float64

Additional Context

If this is due to some numerical issue, I would like to understand what is happening and if there is some tolerance value that I can change to bypass this problem.

Hi @claudia-hm sorry for the late reply. I'm looking into this. First thing I notice is a peculiar statsmodels warning when I enable the trace on the fit:

In [15]: model = pm.auto_arima(y2_train, trace=5)

Performing stepwise search to minimize aic

/opt/miniconda3/envs/ml/lib/python3.7/site-packages/statsmodels/tsa/statespace/sarimax.py:1890: RuntimeWarning: divide by zero encountered in reciprocal

return np.roots(self.polynomial_reduced_ar)**-1

ARIMA(2,1,2)(0,0,0)[0] intercept : AIC=-1614.762, Time=0.07 sec

First viable model found (-1614.762)

ARIMA(0,1,0)(0,0,0)[0] intercept : AIC=-1670.667, Time=0.06 sec

New best model found (-1670.667 < -1614.762)

ARIMA(1,1,0)(0,0,0)[0] intercept : AIC=-1665.984, Time=0.03 sec

ARIMA(0,1,1)(0,0,0)[0] intercept : AIC=15212.220, Time=0.05 sec

ARIMA(0,1,0)(0,0,0)[0] : AIC=-1839.861, Time=0.02 sec

New best model found (-1839.861 < -1670.667)

ARIMA(1,1,1)(0,0,0)[0] intercept : AIC=-1663.997, Time=0.04 sec

Best model: ARIMA(0,1,0)(0,0,0)[0]

Total fit time: 0.276 seconds

I'll dig more into this.

Looks like it still presents even with the latest statsmodels (0.14.0) when using the default optimizer ('lbfgs'):

File "statsmodels/tsa/statespace/_representation.pyx", line 1373, in statsmodels.tsa.statespace._representation.dStatespace.initialize

File "statsmodels/tsa/statespace/_representation.pyx", line 1362, in statsmodels.tsa.statespace._representation.dStatespace.initialize

File "statsmodels/tsa/statespace/_initialization.pyx", line 288, in statsmodels.tsa.statespace._initialization.dInitialization.initialize

File "statsmodels/tsa/statespace/_initialization.pyx", line 406, in statsmodels.tsa.statespace._initialization.dInitialization.initialize_stationary_stationary_cov

File "statsmodels/tsa/statespace/_tools.pyx", line 1525, in statsmodels.tsa.statespace._tools._dsolve_discrete_lyapunov

numpy.linalg.LinAlgError: LU decomposition error.

Seems like changing the optimizer method makes a difference:

In [23]: model = pm.auto_arima(y2_train, method='nm')

In [24]: forecasts = model.predict(y2_test.shape[0])

In [25]: forecasts

Out[25]:

80 0.000280

81 0.000281

82 0.000281

83 0.000282

84 0.000283

85 0.000284

86 0.000285

87 0.000286

88 0.000287

89 0.000288

90 0.000289

91 0.000290

92 0.000291

93 0.000292

94 0.000293

95 0.000294

96 0.000295

97 0.000296

98 0.000297

99 0.000298

dtype: float64

I tried the following and they also appeared to work without issue:

-

powell -

bfgs